The SBTi Corporate Net-Zero Standard v2's Ongoing Emissions Responsibility (OER) Framework

A Guide to the SBTi's New Framework

Understanding how the Corporate Net-Zero Standard v2.0 addresses responsibility for ongoing emissions during the transition to net zero

What is Ongoing Emissions Responsibility?

For more than a decade, the Science Based Targets initiative (SBTi) has been the world's leading framework for corporate decarbonisation. Its core principle has remained unchanged: companies must reduce emissions within their own operations and value chains in line with climate science, and progress toward targets is measured using reductions in their actual greenhouse gas inventory.

Yet even companies that are reducing emissions rapidly continue to generate greenhouse gas emissions throughout the transition to net zero. A company may be aligned with a 1.5°C pathway and still emit millions of tonnes of greenhouse gases each year. Until now, the SBTi framework has largely focused on how quickly those emissions should be reduced. The Corporate Net-Zero Standard v2.0 introduces a new concept intended to address a different question: what responsibility should companies take for the emissions that remain?

The answer is Ongoing Emissions Responsibility (OER). OER is a new recognition framework that sits alongside, rather than replaces, science-based targets. It does not alter target-setting requirements, and participation in OER does not allow companies to use carbon credits or other OER activities in place of emissions reductions when assessing progress toward Scope 1, Scope 2 or Scope 3 targets. Companies must still achieve their science-based targets through emissions reductions within their value chains. OER addresses a separate issue: support for climate action beyond the value chain while those emissions continue to occur.

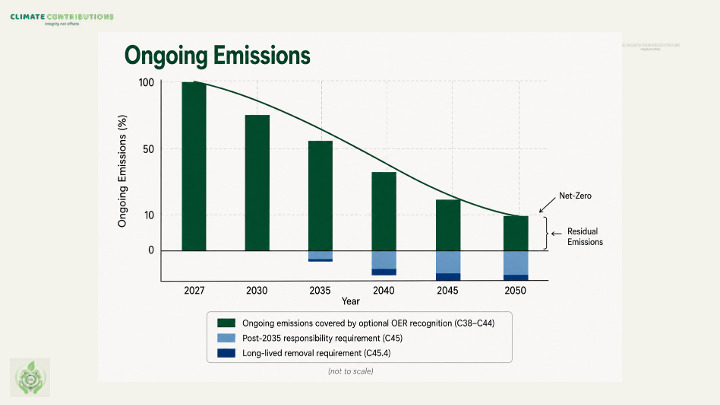

As illustrated below, the OER framework extends beyond the optional recognition programme that has received most attention since the release of the Corporate Net-Zero Standard v2.0. Chapter 6 establishes a broader progression of responsibility over time.

The first phase is the optional OER recognition programme, which allows companies to demonstrate responsibility for a defined share of their ongoing emissions through climate contributions. This is the element of the framework that takes effect immediately and is the primary focus of this article.

The second phase begins in 2035, when Category A companies become subject to a post-2035 responsibility requirement. The third phase applies at the net-zero target year, when all residual emissions must be neutralised using eligible carbon removals.

This article focuses on the optional recognition programme and the mechanisms through which companies can participate in it. Future articles will examine the post-2035 responsibility requirement and the neutralisation provisions in greater detail.

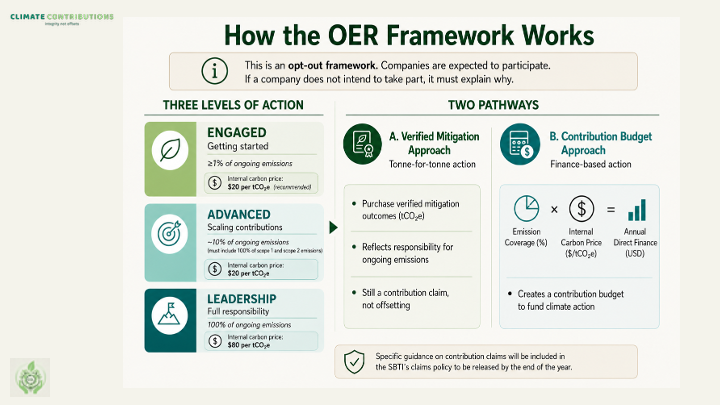

The framework is structured as an opt-out recognition system rather than a purely voluntary add-on. Under CNZS v2.0, companies validating targets must declare whether they intend to participate in OER. Companies choosing not to participate are expected to explain that decision. Companies that do participate may receive recognition under the programme according to the level of responsibility they assume for their ongoing emissions.

How the OER Framework Works

The framework combines two recognised approaches for taking responsibility with three levels of recognition. Together, these determine how much responsibility a company assumes for its ongoing emissions and how that responsibility is translated into climate action.

Two approaches for taking responsibility

The final standard recognises two different approaches through which companies can take responsibility for ongoing emissions.

The first is the Verified Mitigation Approach. Under this approach, companies support verified mitigation outcomes equivalent in volume to the emissions coverage they wish to take responsibility for. In practice, this will often involve supporting high-integrity carbon credits, measured in tonnes of carbon dioxide equivalent (tCO₂e).

The second is the Contribution Budget Approach. Rather than matching emissions with tonnes of mitigation, companies establish a climate contribution budget by applying an internal carbon price to the percentage of their ongoing emissions they wish to take responsibility for. The resulting budget can then be directed toward a broader portfolio of eligible climate actions, including verified mitigation outcomes, ex-ante mitigation funding, low- and zero-carbon research and innovation, mitigation-enabling activities, adaptation and resilience, and loss and damage finance.

By recognising both approaches, the framework creates two distinct pathways through which companies can translate responsibility for ongoing emissions into real-world climate action. One is based on quantified mitigation outcomes, while the other is based on mobilising climate finance through a defined contribution budget.

Three levels of recognition

Recognition is awarded at three levels: Engaged, Advanced and Leadership. These levels are primarily distinguished by the proportion of ongoing emissions covered by the company's climate contributions.

The standard describes the levels as follows:

- Engaged: responsibility for 1% of total ongoing emissions.

- Advanced: responsibility for 10% of total ongoing emissions, including 100% of Scope 1 and Scope 2 emissions.

- Leadership: responsibility for 100% of total ongoing emissions for Category A companies, or 10% of total ongoing emissions (including 100% of Scope 1 and Scope 2 emissions) for Category B companies.

Importantly, the delivery requirements vary across the three levels. Companies seeking Engaged or Advanced recognition may use either the Verified Mitigation Approach or the Contribution Budget Approach. Leadership recognition requires both approaches to be applied simultaneously. Companies must establish a contribution budget based on an internal carbon price and also support verified mitigation outcomes equivalent to the emissions covered.

This distinction reflects the role that Leadership plays within the architecture of the framework. The standard describes Leadership as representing the “full internalization of the cost of climate change” and encourages companies to work toward this level of ambition over time.

The final standard establishes the recognition framework but does not yet define the specific claims associated with each recognition level or delivery approach. The SBTi has indicated that detailed guidance on OER-related claims will be included in a separate Claims Policy, expected to be released by the end of 2026. Until that guidance is published, the framework establishes how companies may take responsibility for ongoing emissions, while the precise language that companies may use to communicate those actions remains under development.

How Large Could the OER Framework Become?

While the final OER framework was only formally adopted as part of the Corporate Net-Zero Standard v2.0 in 2026, the concepts underpinning it have been under development for several years.

The framework builds on a broader evolution in thinking about ongoing emissions since the original Corporate Net-Zero Standard, culminating in the SBTi's Above and Beyond report (2024), and a growing body of work on climate contributions and responsibility for ongoing emissions.

The final standard was also shaped through extensive consultation, expert working groups, company engagement and pilot testing. As a result, OER should not be viewed as a new or untested concept, but rather as the formalisation of ideas that have been under active development across the climate community for several years.

Many of the underlying mechanisms already exist within corporate practice. Hundreds of companies already use internal carbon pricing, while a growing number of companies have begun supporting climate action through contribution-style approaches that sit alongside their decarbonisation strategies. The OER framework builds on these existing practices by providing a common structure through which responsibility for ongoing emissions can be recognised and disclosed.

The scale of future participation remains uncertain and will ultimately depend on company decisions, investor expectations, evolving claims guidance and broader market acceptance. However, there are also strong reasons to expect meaningful uptake. The framework has been shaped through extensive company engagement, responds to growing interest in climate contribution approaches, and builds on tools and practices that many companies already use.

The framework also benefits from being embedded within the world's leading corporate climate standard. More than 13,000 companies have set targets or commitments through the SBTi, creating a large existing user base from which future OER participation could emerge. While participation in OER remains optional, the standard's opt-out structure, recognition system and integration within target validation processes are all designed to encourage engagement rather than treat OER as a stand-alone voluntary initiative.

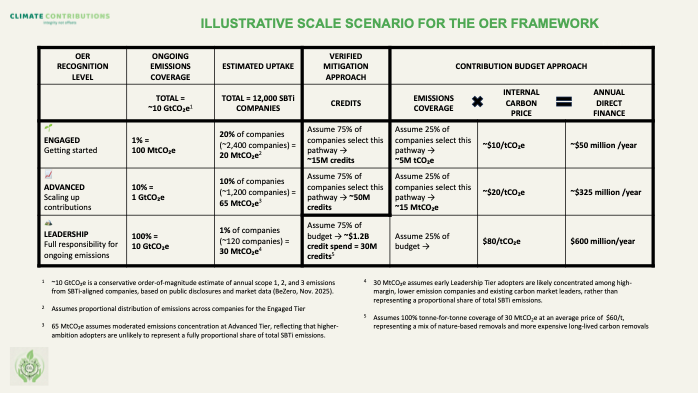

The illustration below presents an indicative scale scenario based on publicly available estimates of emissions associated with SBTi-aligned companies, combined with illustrative assumptions regarding participation across the Engaged, Advanced and Leadership recognition levels. It should not be interpreted as a forecast. Rather, it provides an indication of the order of magnitude of climate finance and verified mitigation demand that could emerge if the framework achieves meaningful adoption.

The scenario presented above is intentionally conservative and should be interpreted as an illustration of potential scale rather than a forecast.

Several assumptions have been deliberately chosen to avoid overstating the framework's potential impact. First, the analysis assumes that SBTi companies are collectively responsible for approximately 10 GtCO₂e of annual emissions. This is substantially lower than some recent estimates and therefore provides a cautious starting point for the analysis.

Second, participation assumptions are deliberately modest. The scenario assumes that only 20% of companies pursue Engaged recognition, 10% pursue Advanced recognition and just 1% pursue Leadership recognition. In total, this implies participation by only 31% of SBTi-aligned companies, despite pilot testing suggesting interest from a substantially larger share of participants.

Third, the analysis assumes that higher-recognition participants are not representative of average corporate emissions. Companies pursuing Advanced and especially Leadership recognition are assumed to have lower-than-average ongoing emissions relative to the wider SBTi population, reducing the overall volume of emissions covered by the framework.

Finally, the scenario assumes relatively limited uptake of the Contribution Budget Approach, with only 25% of participating companies selecting that pathway. For Leadership companies, it also assumes that most available resources are directed toward verified mitigation outcomes before any remaining funds are allocated through a contribution budget.

Taken together, these assumptions are designed to produce a cautious order-of-magnitude estimate. Even under these conservative conditions, the framework has the potential to mobilise substantial additional resources for climate action while generating demand for significant volumes of verified mitigation outcomes.

Importantly, those resources need not flow exclusively toward carbon credits. The Contribution Budget Approach explicitly recognises a broader set of eligible climate actions, including mitigation-enabling activities, innovation, adaptation and resilience, and loss and damage finance.

The significance of the framework therefore lies not only in the scale of resources that could be mobilised, but also in the flexibility with which those resources may be deployed. For the first time, the SBTi has established a formal mechanism through which companies can recognise responsibility for ongoing emissions while supporting a diverse portfolio of climate actions beyond their value chains.

This raises an important question: if companies increasingly adopt the Contribution Budget Approach, where might those resources be directed, and what types of climate action could be supported? The next article explores the Contribution Budget Approach in greater detail and examines its potential implications for climate finance.